Compound interest is one of the most critical factors that influence the repayment of loans. Whether you’re planning to take out a mortgage, a personal loan, or any other type of credit, understanding how compound interest works is essential to managing your finances effectively. In the context of a two-lakh personal loan, it is especially important to grasp how compound interest can impact your total repayment amount and overall financial health.

This article explains the concept of compound interest and its implications on loan repayment, with insights into strategies to minimize its effects on your debt.

What is Compound Interest?

Compound interest is the interest on a loan or deposit that is calculated based not only on the principal amount but also on the accumulated interest from previous periods. Unlike simple interest, where only the principal amount earns interest, compound interest ensures that interest is compounded over time, leading to exponential growth in repayment.

For borrowers, this means the debt keeps increasing as interest accrues. While the principal initially forms the basis for calculation, the compounding mechanism makes the total repayment much larger over time.

Compound Interest vs. Simple Interest

Understanding the difference between compound interest and simple interest is critical when measuring the benefit or burden of borrowing.

Simple Interest

Calculated using a straightforward formula:

Simple Interest = Principal x Rate x Time

With simple interest, the borrower pays interest only on the principal.

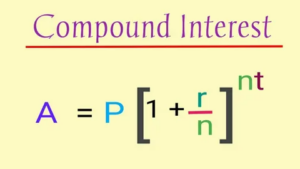

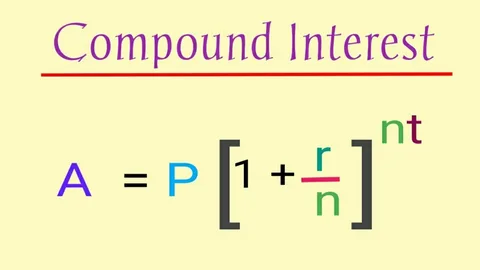

Compound Interest

Calculated using the formula:

Compound Interest = Principal x (1 + Rate/N) ^ (N x Time)

Here, ‘N’ refers to the number of compounding periods per year (quarterly, monthly, etc.). The compounding mechanism significantly increases the amount owed over time due to interest being calculated on both the principal and accrued interest.

For example, when repaying a two-lakh personal loan, compound interest will have a greater impact than simple interest as it compounds periodically, adding up to a larger repayment sum.

How Compound Interest Affects Your 2 Lakh Personal Loan

If you borrow 2 lakh personal loan, compound interest can push your total repayment much higher than originally anticipated. To better understand its effect, consider the following elements:

1. Rate of Interest

The interest rate is the primary driver of the compound interest amount. With a higher interest rate, a larger amount will be compounded and added to your repayment obligations. Even small differences in the interest rate—say 10% versus 12%—can result in thousands of rupees of additional repayment.

2. Loan Tenure

Compound interest grows exponentially over time. Loans with longer tenures are more impacted by compounding. For example, a 10-year loan with monthly compounding will cost substantially more than a 5-year loan at the same rate of interest.

3. Frequency of Compounding

Whether your loan compounds daily, monthly, quarterly, or annually influences how much interest accrues on your debt. Monthly compounding is common for personal loans and results in higher repayment amounts compared to annual compounding.

4. Total Repayment Amount

The total repayment for your two-lakh personal loan will include both the principal and compounded interest. For example, if your loan compounds monthly at a 12% annual interest rate over five years, you could end up repaying significantly more than just ₹2,00,000.

The Math Behind Compound Interest

To illustrate the impact of compound interest on your two-lakh personal loan, consider the following scenario:

Loan Parameters

- Loan Principal: ₹2,00,000

- Annual Interest Rate: 12%

- Loan Tenure: 5 years

- Monthly Compounding

Formula

Using the compound interest formula:

A = P × (1 + r/n)^(n × t)

Where:

- A = Total repayment amount

- P = Principal amount (₹2,00,000)

- r = Annual interest rate (12% or 0.12)

- n = Number of compounding periods per year (12 for monthly compounding)

- t = Loan tenure in years (5 years)

Calculation Steps

A = 200,000 × (1 + 0.12/12)^(12 × 5)

A = 200,000 × (1 + 0.01)^60

A = 200,000 × 1.819397

A = ₹3,63,879

In this example, the total repayment for your ₹2,00,000 loan would be ₹3,63,879, meaning you pay ₹1,63,879 in interest alone over five years.

Strategies to Reduce the Impact of Compound Interest

While compound interest makes borrowing more expensive, there are ways to minimize its impact:

1. Negotiate a Lower Interest Rate

Shop around for competitive rates before taking out a two-lakh personal loan. Even small reductions in the interest rate can save you thousands over the loan term.

2. Opt for Shorter Loan Tenures

A shorter loan tenure will accumulate less interest, as the compounding effect has less time to grow. While monthly payments may be higher for shorter tenures, the overall repayment will be lower.

3. Make Prepayments

Paying off part of the loan early reduces the principal amount on which interest is calculated. This can significantly lower your total repayment, especially in loans where compound interest plays a role.

4. Choose Loans with Less Frequent Compounding

If possible, select loans that compound annually instead of monthly or quarterly. Less frequent compounding translates to lower total interest costs.

The Power of Financial Planning

Understanding compound interest can help you make informed decisions about your borrowing needs. Whether you need a two-lakh personal loan for medical expenses, education, or home improvement, evaluating the repayment terms carefully can save you a lot of money.

Planning ahead, negotiating lower rates, and making prepayments are essential tools to reduce the impact of compound interest. Additionally, using loan calculators to simulate repayment scenarios can give you a clear picture of the costs involved, enabling you to budget effectively.

Conclusion

Compound interest is a powerful factor that significantly affects your total repayment on loans, including personal loans. Its exponential growth means borrowers often pay much more than anticipated, especially for long-term debt. A ₹2,00,000 personal loan with monthly compounding can result in a total repayment far exceeding the principal amount, making it essential to understand its implications fully.

By negotiating better interest rates, opting for shorter tenures, and making prepayments, you can minimize the impact of compound interest on your borrowing costs. Armed with knowledge and careful financial planning, you can reduce your financial burden and maintain greater control over your finances.